What Is Net Revenue Retention?

Net revenue retention (NRR) measures how much revenue you keep and grow from your existing customers over a given period — typically 12 months. It accounts for expansion revenue (upsells, cross-sells, seat growth), contraction (downgrades), and churn (cancellations). An NRR of 120% means your existing customer cohort generates 20% more revenue this year than last year — before you add a single new customer.

NRR has become the single most scrutinized metric in SaaS. Investors, board members, and operators all agree: it’s the clearest signal of product-market fit, pricing health, and long-term SaaS growth potential. A company with 120% NRR effectively doubles its existing revenue base every 3.8 years without acquiring any new customers. That’s compounding at its most powerful.

The NRR Formula

The formula is straightforward:

Net Revenue Retention Rate

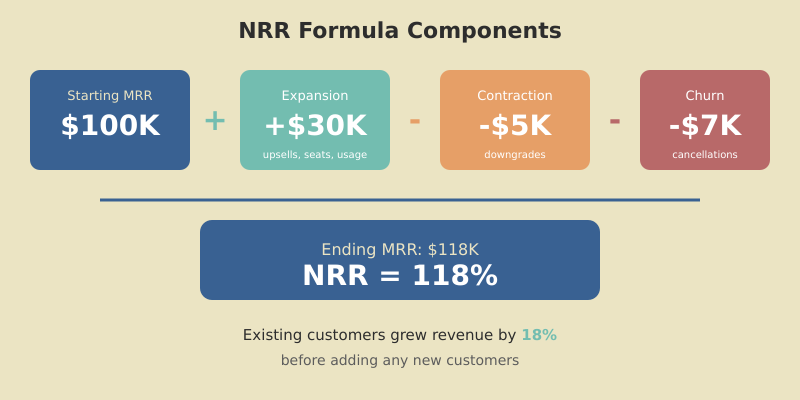

NRR = (Starting MRR + Expansion – Contraction – Churn) / Starting MRR × 100

Let’s break that down with a real example:

| Component | Amount | What It Means |

|---|---|---|

| Starting MRR (Jan) | $100,000 | Revenue from existing customers at period start |

| + Expansion | +$30,000 | Upgrades, added seats, usage growth |

| – Contraction | -$5,000 | Downgrades to lower plans |

| – Churn | -$7,000 | Customers who cancelled |

| Ending MRR | $118,000 | Net result |

| NRR | 118% | ($118K / $100K) × 100 |

NRR vs. GRR: What’s the Difference?

NRR and gross revenue retention (GRR) are related but answer different questions:

| Metric | Includes Expansion? | Can Exceed 100%? | What It Tells You |

|---|---|---|---|

| NRR | Yes | Yes — 120%+ is great | Overall revenue health of existing customers |

| GRR | No | No — 100% is the ceiling | Your retention floor (how leaky is the bucket?) |

Think of GRR as the foundation — it shows whether you’re keeping customers. NRR shows whether you’re growing them. You need both. A company with 130% NRR but 70% GRR is growing through expansion but hemorrhaging customers, which is unsustainable. The best SaaS companies have GRR above 90% and NRR above 115%.

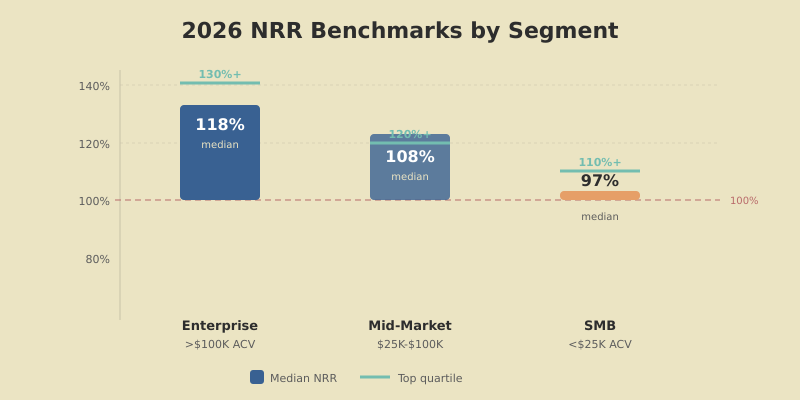

2026 NRR Benchmarks by Segment

NRR varies dramatically by customer segment. Enterprise customers expand more but also take longer to close — and when they churn, it hurts more. Here are the current benchmarks from m3ter’s 2026 SaaS valuation analysis:

| Segment | ACV | Median NRR | Top Quartile |

|---|---|---|---|

| Enterprise | >$100K | 118% | 130%+ |

| Mid-Market | $25K–$100K | 108% | 120%+ |

| SMB | <$25K | 97% | 110%+ |

The valuation premium

A 10-point NRR increase can boost SaaS valuation by 20–30%. That’s because high NRR compounds — every dollar of ARR generates more revenue over time. Investors pay premium multiples for companies where the existing customer base grows itself.

The 5 Levers to Hit 120%+ NRR

Getting from 100% to 120% NRR requires pulling five levers simultaneously. I’ll walk through each one in order of impact.

Lever 1: Fix Your Retention Floor First

You can’t out-expand bad retention. If your churn rate is eating 10%+ of revenue annually, expansion revenue is just filling a leaky bucket. Get GRR to 90%+ before investing in expansion.

Focus areas:

- Reduce involuntary churn — failed payments and expired cards cost 2–5% of ARR annually. Implement dunning emails, card updaters, and payment retry logic

- Fix onboarding — customers who activate quickly churn less. Track time-to-value and remove friction from the first 14 days

- Run churn surveys — identify the top 3 reasons customers leave and systematically address them

Lever 2: Design Pricing That Scales with Value

Your pricing model is the most powerful NRR lever. If customers get 10x more value as they grow but your pricing stays flat, you’re leaving expansion revenue on the table.

The best pricing models for NRR:

Usage-based pricing

Revenue scales automatically with customer usage. No sales intervention required. Companies with usage-based pricing routinely post 120%+ NRR because expansion happens organically. Example: Twilio, Snowflake, AWS.

Seat-based pricing

Revenue grows as teams add users. Works best for collaboration tools where the product gets more valuable with more people. Example: Slack charges per active user — as teams grow, revenue follows.

Tiered feature pricing

Customers upgrade to higher tiers for advanced features. Works when you have clear feature differentiation between plans. Risk: customers may stay on lower tiers if the upgrade value isn’t obvious enough.

Lever 3: Build Product-Led Expansion

The most scalable expansion comes from the product itself — not from sales outreach. Surface upgrade opportunities naturally within the user experience:

- Usage limit nudges — “Your team has used 85% of your monthly data. Upgrade for unlimited access”

- Feature discovery — show premium features with a “Pro” badge and a one-click upgrade path

- Team growth triggers — when users invite colleagues, prompt them to consider team plans

- Value milestones — “You’ve saved 40 hours this month with automation. See what the Pro plan unlocks”

As McKinsey’s B2B tech research shows, companies with the most sophisticated value realization journeys produce NRR about seven percentage points higher than peers with basic practices.

Lever 4: Invest in Proactive Customer Success

Customer success teams should own expansion revenue targets alongside retention. The best CS organizations generate 30–50% of total expansion revenue through proactive account management.

Key CS practices for NRR:

- Quarterly business reviews (QBRs) — show customers the value they’ve received and identify growth opportunities

- Health scores — flag at-risk accounts before they churn and high-usage accounts before they outgrow their plan

- Onboarding milestones — align with customers on clear adoption goals in the first 30/60/90 days

- Usage-based triggers — when an account hits 80% of tier limits, CS proactively reaches out with upgrade recommendations

Lever 5: Add Dedicated Expansion Sales

For companies with NRR above 115%, consider dedicating expansion roles rather than having account managers handle both retention and growth. Specialization typically increases expansion deal velocity by 25–40%.

Expansion sales is different from new business sales. The customer already uses your product. The expansion rep’s job is to identify accounts with growth potential, map expansion opportunities (more seats, higher tier, additional products), and close upsell deals — all informed by usage data that new business reps don’t have.

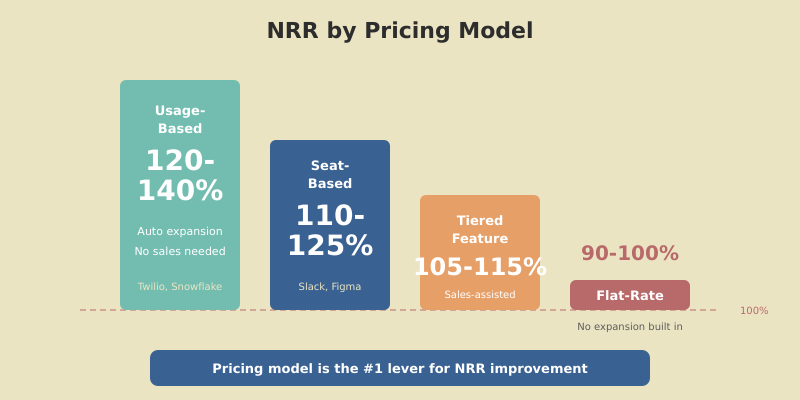

NRR by Pricing Model

Your pricing model has the largest single impact on achievable NRR. Here’s what I’ve seen across different pricing structures:

| Pricing Model | Typical NRR | Expansion Mechanism | Best For |

|---|---|---|---|

| Usage-based | 120–140%+ | Automatic — revenue scales with usage | APIs, infrastructure, data |

| Seat-based | 110–125% | Semi-automatic — grows with team | Collaboration, productivity |

| Tiered feature | 105–115% | Sales-assisted — requires upgrade decision | Broad SaaS platforms |

| Flat-rate | 90–100% | None built-in — relies entirely on upsells | Avoid for NRR growth |

FAQ

What is a good net revenue retention rate for SaaS?

For enterprise SaaS (ACV >$100K), target 115–130%+ NRR. For mid-market ($25K–$100K), 105–120% is strong. For SMB (<$25K), 100–110% is good. Any NRR below 100% means your existing customer base is shrinking, which signals fundamental retention issues that must be addressed first.

What is the difference between NRR and GRR?

GRR (gross revenue retention) measures revenue kept from existing customers excluding expansion — it caps at 100% and shows your retention floor. NRR includes expansion revenue so it can exceed 100%. GRR reveals how well you retain; NRR reveals how well you retain and grow. Both matter — target 90%+ GRR and 115%+ NRR.

How does pricing model affect NRR?

Usage-based pricing consistently produces the highest NRR (120–140%+) because expansion happens automatically as customers use more. Seat-based pricing achieves 110–125% through team growth. Tiered feature pricing typically produces 105–115%. Flat-rate pricing caps NRR near 100% since there is no built-in expansion mechanism.

Should I focus on reducing churn or increasing expansion?

Fix churn first. If your GRR is below 90%, focus all efforts on reducing churn and contraction before investing in expansion strategies. High expansion with high churn is unsustainable — you are replacing lost customers rather than growing. Once GRR reaches 90%+, layer in expansion initiatives for sustainable NRR growth.

How does NRR affect SaaS company valuation?

NRR is one of the strongest valuation drivers in SaaS. A 10-point NRR improvement can increase company valuation by 20–30%. Investors pay premium multiples for high-NRR companies because the existing customer base generates compounding revenue growth, reducing dependence on expensive new customer acquisition.

Start Improving Your NRR Today

Net revenue retention isn’t just a metric — it’s the compound interest of SaaS. Every percentage point above 100% compounds over time, building a revenue engine that grows whether or not you add new customers.

Here’s where to start: calculate your current NRR and GRR. If GRR is below 90%, focus on retention — reduce involuntary churn, fix onboarding, and address the top reasons customers leave. If GRR is healthy, shift to expansion: redesign pricing to scale with customer value, build product-led expansion triggers, and invest in proactive customer success.

For the broader context on how NRR fits into your SaaS growth strategy, check our complete guide. And if churn is your primary blocker, our SaaS churn benchmarks article breaks down what’s acceptable and what needs fixing.